Looking for business debt relief services? Visit Delancey Street.

–

Dealing with business debt can be overwhelming. Unpaid bills pile up, creditors call nonstop, and you feel like you’re drowning with no relief in sight. But there are solutions available to find your way out of debt, restore your financial health, and move forward on steadier ground. Business debt settlement is one potential path to resolve what you owe and make a fresh start.

What is Business Debt Settlement?

Business debt settlement involves working with a debt settlement company to negotiate with your creditors to pay less than the full amount you owe. The goal is to come to an agreement to settle accounts for a lump sum payment that is more affordable for you. This allows you to resolve debt, avoid bankruptcy, and continue operating your business.Here’s a quick rundown of how the debt settlement process typically works:

- You stop making payments to creditors and instead save money in a secure account. This helps show you’re making an effort to pay what you can.

- The settlement company negotiates with creditors on your behalf to reduce the balances. Often they can get accounts cut by 40-60%.

- You pay the negotiated, reduced amount as a one-time lump sum payment to settle each debt.

- The creditor agrees to forgive the remaining balance and close the account.

Settling debt means you don‘t have to pay the full amount owed. This can save a struggling business tens of thousands of dollars and provide major relief.

Key Benefits of Business Debt Settlement

There are many advantages to settling your business debts compared to other debt solutions:

- Pay Less Than You Owe – With successful negotiations, you can have debt balances cut significantly and avoid paying interest and late fees. This protects valuable assets.

- Avoid Bankruptcy – Settling debt lets you resolve what you owe while keeping your business open. This beats the major disruptions of filing bankruptcy.

- Become Debt Free – Completing the negotiated settlements allows you to resolve accounts completely and not owe creditors anything more. This gives you a fresh slate.

- Improve Cash Flow – With less debt expense every month, more money can go toward operating costs. This helps stabilize finances.

- Stop Collection Calls – Once debts are settled, creditors stop the harassing calls demanding money. This reduces stress and headaches.

Settling debt can resolve unmanageable financial obligations in an affordable way while protecting your business.

Step 1: Review Finances for Settlement Potential

The first step is to review your business finances to gain clarity on all outstanding debts. This allows us to understand the full scope of what is owed so we can provide tailored advice for your situation.We will conduct an in-depth analysis of all owed balances, minimum payments, interest rates, late fees, creditors‘ collection actions, and other key factors. This helps determine if settlement is the right solution.Key questions we analyze:

- How much total business debt do you currently have?

- What types of debt make up this amount (loans, credit cards, vendors, etc.)?

- How much are the monthly payments toward debt?

- How does this debt expense impact your cash flow?

- Which creditors are most aggressively pursuing collections?

Compiling this financial profile allows us to give specific settlement recommendations for your unique situation.

Step 2: Open Settlement Account & Stop Paying Creditors

If settlement is advised, the next step is opening a dedicated savings account that will be used to eventually pay your negotiated lump sum settlements.You would also immediately stop making monthly payments to all creditors included in the program. This is a vital piece of showing you cannot reasonably pay back the full balances.The funds you were paying toward debt will instead go into the settlement account. When that account reaches sufficient funds to offer reasonable settlement amounts, negotiations with creditors begin.

Step 3: Negotiate with Creditors

Experienced debt settlement experts will contact your creditors on your behalf and negotiate to settle accounts for less than you owe. The first priority is discussing accounts where creditors are aggressively attempting collections or legal actions that could seriously disrupt business operations.The negotiation process aims to have 40-60% (or more in some cases) cut from your debt. This is made possible by highlighting key aspects like:

- You are facing serious financial hardship in keeping up with payments

- You have funds available to offer as a lump sum settlement, but cannot maintain monthly payments

- Accepting a reduced settlement is better for the creditor than receiving nothing if you go bankrupt

Several rounds of negotiation may be needed before an acceptable settlement amount can be agreed to by both you and the creditor. Patience is key, as is maintaining funds in your settlement account so you can show creditors you have money available to pay in a lump sum.

Step 4: Settle Debt Accounts

As negotiations wrap up and specific settlement terms are reached, you would pay the agreed-upon reduced lump sums from your dedicated savings account. Creditors accept payment as resolution of that account.You must get any settlement details formally in writing from the creditor before paying. This acts as a record that your debt obligation is considered fulfilled and legally satisfied once they receive the negotiated payoff amount.As you settle each account, creditors stop all collection efforts, waive remaining balances, and close accounts. This helps you make clean breaks from previously unmanageable debt burdens.

How Much Could Debt Settlement Save My Business?

Savings from settling your business debt really depend on specific factors like:

- How much you currently owe across various accounts

- Types of debt (high-interest credit cards, vendor bills, equipment leases, etc.)

- Success of negotiations with individual creditors

- How much available settlement funds you have to offer

But generally, settled debt saves a business significant money compared to paying accounts in full. Here is a basic example:

- Owed: $100,000 across 10 credit cards and vendor accounts

- Monthly Payments: $4,500

- Interest: Varies by account between 12-29% APR

If settled at 50% discounts, you would pay $50,000 as a lump sum to resolve all $100k owed. This is a $50,000 savings, at minimum.And avoiding interest fees going forward saves money each month. That means more cash flow funding operations rather than paying debt.

Why Business Debt Settlement is Better Than Bankruptcy

Another option some companies consider when facing unmanageable debt is declaring business bankruptcy. However, there are major downsides as bankruptcy can seriously disrupt operations.

- Company Closure – The bankruptcy process may require halting business activity completely. This can permanently damage operations.

- Asset Seizure – A court can order the seizure and sale of key business assets to pay creditors. This loss of property can severely inhibit financial recovery post-bankruptcy.

- Higher Expenses – Attorney and court fees related to filing bankruptcy can cost tens of thousands of dollars. This diverts money away from funding normal business functions.

- Damaged Credit & Reputation – Business bankruptcy devastates credit scores and remains on reports for years. Vendors/lenders may refuse services going forward due to this red flag.

With business debt settlement, none of these downsides exist. You maintain control of assets, avoid legal expenses, and resolve debt through mutually-beneficial agreements with creditors. This sets you up for financial restoration and continued smooth operations.

What Makes a Business Best Suited for Debt Settlement?

While debt settlement can resolve what many companies owe, the companies best positioned for success meeting settlement terms share certain traits. These include:

Facing Legal Action – If creditors have filed lawsuits or threaten asset seizures, settling may halt those collection attempts. This prevents business stability from being upended.

Strong Cash Flow – Reliable cash flow ensures you can save up sufficient reserve funds to offer reasonable settlement amounts. Without consistent income, the process may falter.

Owe $15k – $250k+ – Businesses with this amount of debt tend to achieve high settlement success and savings. Those with less may find bankruptcy simpler. And those with more owed may struggle to settle within a reasonable timeframe before legal actions escalate.

Flexible Operations – Since settling halts monthly debt payments for a time, maintaining lean operations with variable costs helps endure short-term cash flow shifts while the process runs its course.If your business aligns with these traits, debt settlement could offer an optimal path to resolve debt and provide financial relief.

What Types of Business Debt Can Be Settled?

Many non-secured debts that require ongoing payments on balances owed make good candidates for settlement negotiations. Common examples include:

- Credit Cards – Business credit card debt is an ideal type to settle since cards often carry high interest rates. This priority debt quickly becomes unaffordable.

- Vendor Bills – Money owed to suppliers and contractors can also be negotiated if you cannot realistically pay within terms. Slowing operations may limit reliance on vendors.

- Equipment Leases – Leasing essential items like machinery or fleet vehicles often requires years of payments. Settlement provides lease relief.

- Business Loans – Term loans and SBA loans could potentially be renegotiated and settled below original principal too.

- Commercial Mortgages – If you fall behind on real estate loans, lenders may settle to recoup some money rather than foreclosing.

- Tax Debts – While the IRS does not negotiate directly, settling business tax obligations is possible using an Offer in Compromise submission.

Essentially debts with a past-due balance, accumulating interest/fees, flexible terms, and no collateral tied to the amount can be negotiated for settlement. This encompasses most major non-secured business finance obligations.

What Debts Should Not Be Included?

On the other hand, some types of obligations do not make practical sense to attempt settling. These debts that should not be included are:

Secured Debts – Loans tied to an asset like equipment financing or auto loans that could be repossessed if terms are broken cannot be negotiated through settlement.

Business Renovation Loans – Contractor financing owed for a recent build-out or renovation may have strict repayment requirements without flexibility to settle.

Recent Accounts – Creditors are less likely to settle debt recently taken on though they may negotiate older delinquent accounts more willingly.

Utility Bills – Ongoing electric, gas, water, phone and other recurring operational bills cannot be settled as maintaining service is essential. Payment plans can ease these debts.

Court Judgements – If creditors win lawsuits against your business, that judgement debt involves separate legal standards than typical accounts.The common thread is that these debts all have unique restrictions, collateral obligations, or legal oversight involved that prevents settling – although some alternative options could still improve the obligations.

How Long Does Business Debt Settlement Take?

The duration of the settlement process can vary substantially case-by-case based on total debt, creditors, operational flexibility to stockpile reserves, and pace of successful negotiations. But the timeline typically spans 6-36 months until all accounts are resolved.It takes time to properly prepare documentation, record financial data, open a dedicated account, discuss deals with multiple creditors, and finalize the negotiations. This phased timeline provides a rough guide to expect:

Months 1-3 – Review finances, open settlement account, stop paying unsecured debts

Months 3-6 – Begin negotiations with most pressing creditors

Months 6-12 – Reach initial 1-3 small debt settlements

Months 12-24 – Settle remaining accounts based on available funds

Months 24-36 – Finalize any lingering settlement offers on hardest-to-settle debt

Shoot for settling at least one account within the first 6 months to gain momentum. Also beware that new unexpected debts could arise during the process that may need incorporating into settlement discussions.

How To Get Out Of Small Business Debt | Small Business Debt Relief Options

Business Debt Settlement can put your small business at risk

Beware Of Business Debt Settlement Companies! #debtsettlement #debt #business #lawfirm

Beware of Business Debt Settlement Scams #debtsettlement #businessdebt #merchantcashadvance

To achieve their development goals, African nations urgently need immediate, unconditional debt relief and quick access to new, low-interest financing, perfectly aligned with the Debt-for-Development swaps concept.

Learn more about the concept from our China Development

中国が債務救済への道を開く

https://gesara.news/china-way-debt-relief/

中国人民銀行は新興市場国の債務再編において債権者間の公平な負担分担を求めており、世界の債務問題に積極的な姿勢を示している。

"After leading Medicaid expansion into becoming a reality, Cooper is pushing and prodding the state’s healthcare systems to help in reducing the $4 billion in medical debt owed by North Carolinians." #ncpol

https://greensboro.com/news/local/governor-touts-churchs-medical-debt-relief-efforts-as-model/article_89276b43-f428-5b0e-b801-8a9a2500ad68.html

Pakistan's finance minister in Beijing to seek debt relief, say sources http://reut.rs/3WBy5dn

Biden/Harris

-Unemp 3.7%, 15M new jobs

- student debt relief,$35 Insulin

-American Rescue Plan,Inflation Reduction Act

-First gun law in 30yrs, Killed AlQaeda head

-Confirmed 200 judges

-Strongest NATO alliance ,New Infrastructure bill

-Secured $1.5B from Mexico

-6Mkidsoutofpover

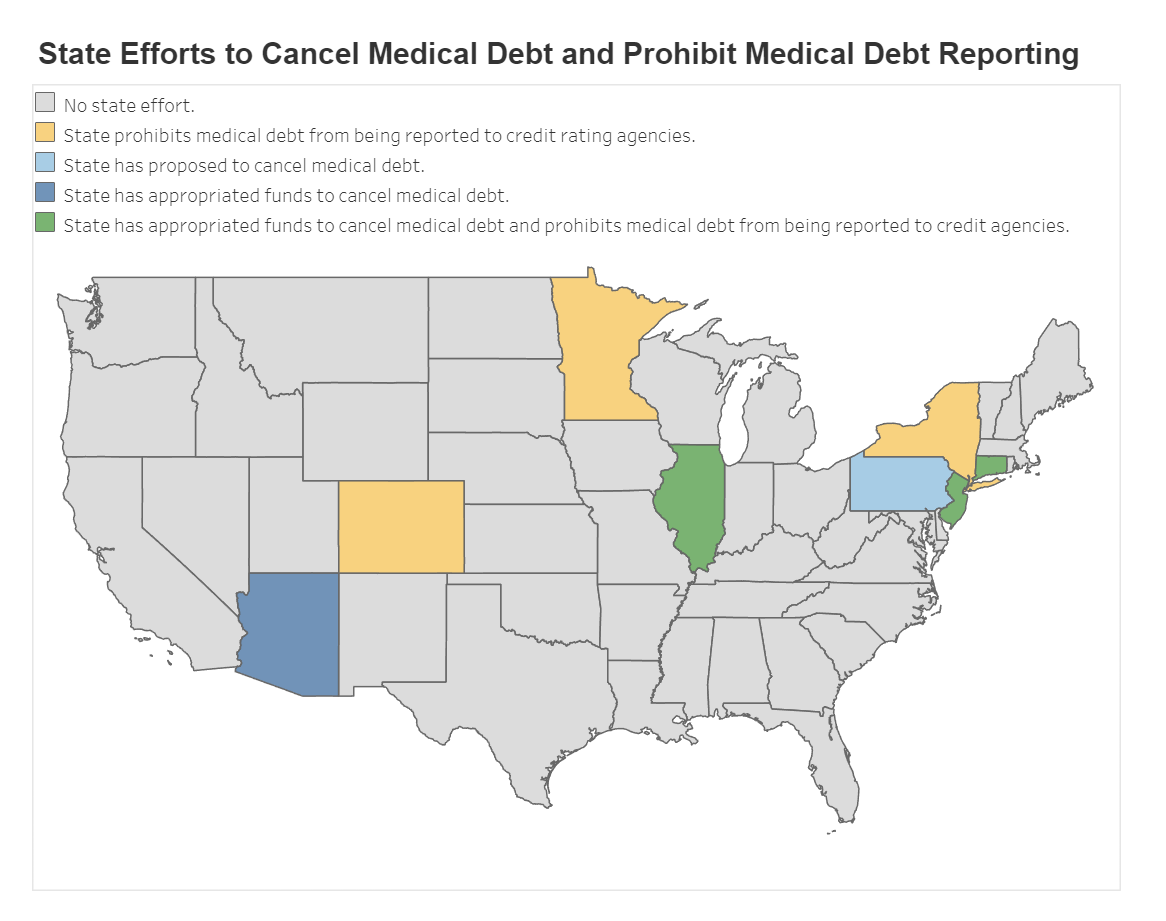

New Jersey is one of only three states in the nation to prohibit medical debt reporting to credit agencies as well as working to provide residents with direct medical debt relief.

We are proud to lead the way in building a health care system that is more affordable and

Student debt relief isn't just a solution; it's a NECESSITY. #CancelStudentDebt

Student debt is a major barrier to #InclusiveGrowth. Let's advocate for affordable education and debt relief programs that allow everyone to thrive. #DebtFreeEducation #GenZ

Last year, we expanded Medicaid, giving more than 600k North Carolinians access to quality, affordable health care. Now, we’re leveraging our Medicaid program to incentivize hospitals to eliminate billions of dollars in medical debt for North Carolinians.

https://www.wbtv.com/2024/07/23/cooper-ncdhhs-hold-round-table-medical-debt-relief/

{kind=link}