Looking for business debt relief services? Visit Delancey Street.

–

Business Debt Settlement: An Overview

Dealing with business debt can be extremely stressful and overwhelming. As a business owner, you may have racked up significant debts – from business loans, to credit cards, to unpaid invoices. The financial pressures can feel inescapable.However, there are options. Business debt settlement may provide a path forward. This article will provide an overview of business debt settlement – what it is, how it works, the pros and cons, and more. We’ll also share actionable tips for navigating the process.

What is Business Debt Settlement?

Business debt settlement involves negotiating with creditors to pay off debts for less than the full amount owed. A business will work with a debt settlement company to put together a settlement offer – usually paying 30-50% of the total debt amount. If creditors accept the offer, the remaining debt is forgiven.For example, if a business owes $100,000 across multiple debts, they may offer creditors $50,000 as full settlement. This allows them to resolve debts they couldn’t otherwise afford to pay.Debt settlement does have risks, which we’ll explore more below. But for many businesses struggling with insurmountable debts, it can provide much-needed relief.

Key Benefits of Business Debt Settlement

There are a few key potential benefits that make business debt settlement an appealing choice:

- Pay Off Debts at a Discount – With debt settlement, businesses can resolve debts for a fraction of what they owe. This makes debts more manageable.

- Avoid Bankruptcy – For deeply distressed businesses, bankruptcy may be the only option. Debt settlement allows businesses to avoid this outcome.

- Stop Collection Activities – Once a debt is enrolled in a settlement program, collection calls and legal actions usually halt. This provides immediate relief.

- Improve Cash Flow – Debt payments are lowered through settlement, freeing up operating cash flow. This allows businesses to reinvest in growth.

For businesses overburdened by debts they can’t afford to pay, settlement may be a financial lifeline. The ability to eliminate debts at a steep discount is often extremely attractive.

An Overview of the Debt Settlement Process

If you decide to pursue business debt settlement, what can you expect? The process generally involves several key steps:

1. Review Debts & Assess Options – First, you’ll thoroughly review all business debts to understand what is owed. It’s critical to assess all options – including bankruptcy, loans/refinancing, or repayment plans – before committing to settlement.

2. Enroll in Settlement Program – Once settlement is selected, you’ll engage a settlement firm and enroll debts into a program. Reputable firms charge fees only on debts successfully reduced – not upfront.

3. Open Settlement Account – You’ll open a dedicated account to save funds to pay settlements. The firm will analyze your finances to determine an appropriate savings timeline – usually 12-48 months.

4. Cease Payments to Creditors – After debts are enrolled, you’ll generally stop making monthly payments to creditors. This helps pressure them to settle debts. However, interests/fees may still accrue.

5. Settlement Firm Negotiates Offers – Once sufficient funds are saved, the settlement firm will negotiate with creditors. This involves back-and-forth communication to reach acceptable offers.

6. Creditors Accept/Reject Offer – If an offer is accepted, you’ll pay the settlement amount from your dedicated account. If rejected, the firm will re-negotiate or wait until more funds accrue.

7. Forgiven Debts Reported on Taxes – Settled debts not paid must be reported as taxable income. Settlement firms can provide guidance on tax implications.While every situation is unique, these steps capture the general process from start to finish. It requires patience, but the rewards can be worthwhile.

Risks and Considerations of Business Debt Settlement

Debt settlement can be an effective resolution strategy – but there are also downsides to consider:

- Settlement Failure – There is no guarantee creditors will accept settlement offers. They may continue collection efforts instead.

- Tax Consequences – Forgiven debts not paid must be claimed as taxable income. This can result in unanticipated tax bills.

- Credit Score Impacts – Missed payments and settled debts will likely devastate business credit scores. This can impair future financing options.

- Balloon Payments – If settlements fail, any remaining debts will come due immediately. Businesses may lack funds to make these balloon payments.

- Interest/Fee Accrual – While settlement is pending, interest and fees may continue accruing. This will increase debts.

While settlement provides the opportunity for steep debt reduction, nothing is guaranteed. Businesses must carefully weigh risks before pursuing this path.

Tips for Navigating Business Debt Settlement

If moving forward with settlement, these tips can help increase the likelihood of success:

- Research Settlement Firms Thoroughly – Many fraudulent or ineffective firms exist. Vet firms properly and read reviews before engaging one.

- Enroll Debts Strategically – Don’t bite off more than you can chew. Be strategic in selecting which debts to enroll to align with business goals.

- Get Tax Advice – Meet with a tax professional to understand tax implications. Settle this year vs next year to optimize write-offs.

- Open Separate Bank Account – Isolate settlement funds in a separate account creditors can’t access. Automate transfers to ensure regular savings.

- Keep Creditors Informed – Maintain open communication with creditors on your situation. This builds goodwill and credibility for settlement offers.

- Be Flexible on Settlement Amounts – Be prepared to increase offers if initial amounts are rejected. Aim high, but have wiggle room to secure deals.

With careful planning and execution, businesses can successfully resolve debts through settlement. But it requires patience and financial discipline throughout what can be a long process.

Is Business Debt Settlement Right For You?

There is no one-size-fits-all approach to business debt relief. Debt settlement offers one potential path that may be appropriate depending on your specific situation.As you weigh options, consider questions such as:

- Is my business truly unable to meet monthly debt obligations? Or could we repay debts if we made sacrifices and cut costs?

- What is our long-term outlook? Do we expect business performance to improve over time?

- How urgent are our issues? Are creditors aggressively pursuing collections or legal action?

- How much risk can we tolerate if settlements fail? Could we withstand balloon payments coming due?

Analyze these dynamics surrounding your debt troubles to determine if settlement aligns with your circumstances and risk tolerance. Consult trusted financial advisors for guidance as well. While settlement can work, other alternatives may better suit some businesses.

Final Thoughts

Navigating heavy business debt is challenging – but know that a path forward is possible. Take time to properly assess your situation and research all options. Business debt settlement may allow you to resolve unaffordable debts for a fraction of what you owe.But be aware of the risks – settlement failure, tax bills, damaged credit, balloon payments. Approach negotiations carefully and have backup plans ready. With eyes wide open to downsides, settlement can offer struggling businesses a lifeline and a fresh start.I’m hopeful this overview equips you to make the most informed choice on how to tackle your business debts. Remember – you don’t have to go it alone. Seek counsel from financial experts every step of the way. There are always solutions for taking control of debt, even when it feels endless. Here’s to your success ahead

How To Get Out Of Small Business Debt | Small Business Debt Relief Options

Business Debt Settlement can put your small business at risk

Beware Of Business Debt Settlement Companies! #debtsettlement #debt #business #lawfirm

To achieve their development goals, African nations urgently need immediate, unconditional debt relief and quick access to new, low-interest financing, perfectly aligned with the Debt-for-Development swaps concept.

Learn more about the concept from our China Development

中国が債務救済への道を開く

https://gesara.news/china-way-debt-relief/

中国人民銀行は新興市場国の債務再編において債権者間の公平な負担分担を求めており、世界の債務問題に積極的な姿勢を示している。

"After leading Medicaid expansion into becoming a reality, Cooper is pushing and prodding the state’s healthcare systems to help in reducing the $4 billion in medical debt owed by North Carolinians." #ncpol

https://greensboro.com/news/local/governor-touts-churchs-medical-debt-relief-efforts-as-model/article_89276b43-f428-5b0e-b801-8a9a2500ad68.html

Pakistan's finance minister in Beijing to seek debt relief, say sources http://reut.rs/3WBy5dn

Biden/Harris

-Unemp 3.7%, 15M new jobs

- student debt relief,$35 Insulin

-American Rescue Plan,Inflation Reduction Act

-First gun law in 30yrs, Killed AlQaeda head

-Confirmed 200 judges

-Strongest NATO alliance ,New Infrastructure bill

-Secured $1.5B from Mexico

-6Mkidsoutofpover

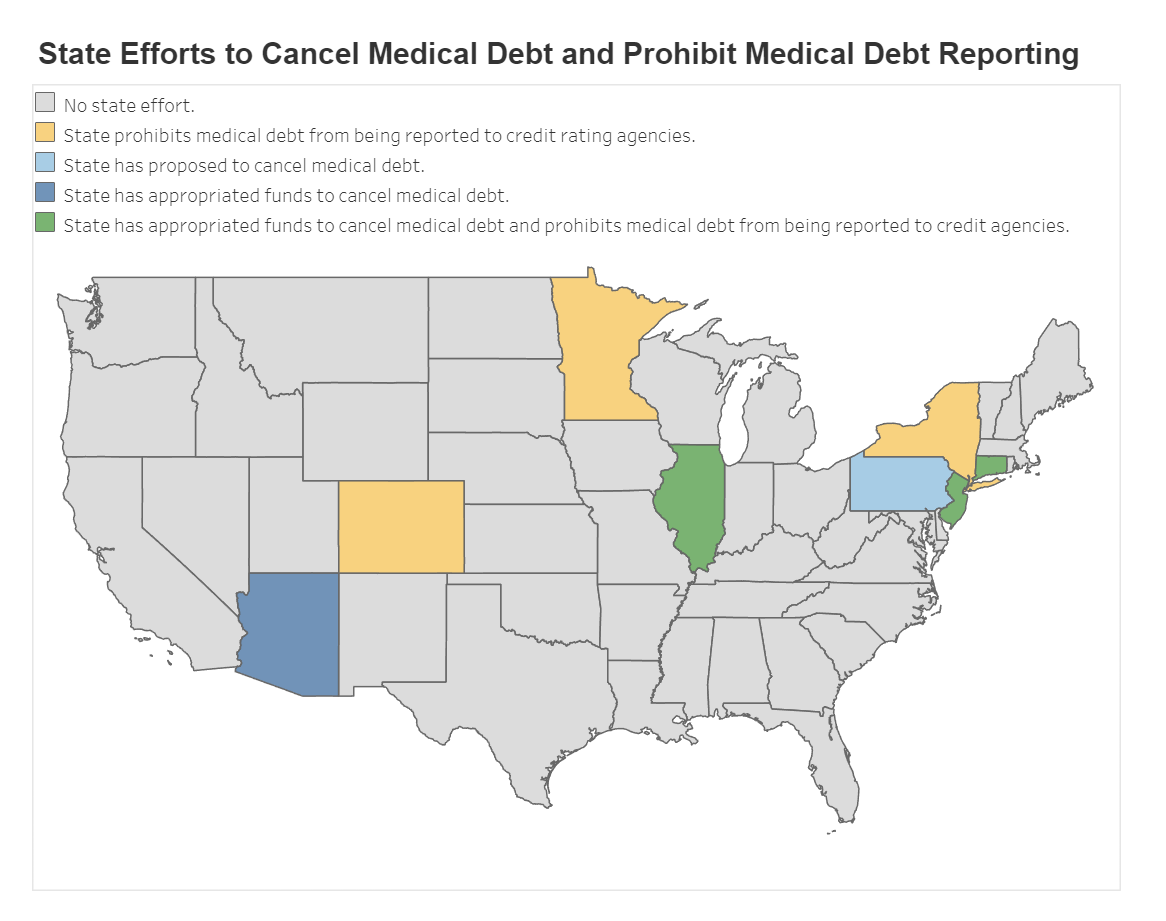

New Jersey is one of only three states in the nation to prohibit medical debt reporting to credit agencies as well as working to provide residents with direct medical debt relief.

We are proud to lead the way in building a health care system that is more affordable and

Student debt relief isn't just a solution; it's a NECESSITY. #CancelStudentDebt

Student debt is a major barrier to #InclusiveGrowth. Let's advocate for affordable education and debt relief programs that allow everyone to thrive. #DebtFreeEducation #GenZ

Last year, we expanded Medicaid, giving more than 600k North Carolinians access to quality, affordable health care. Now, we’re leveraging our Medicaid program to incentivize hospitals to eliminate billions of dollars in medical debt for North Carolinians.

https://www.wbtv.com/2024/07/23/cooper-ncdhhs-hold-round-table-medical-debt-relief/

{kind=link}