Looking for business debt relief services? Visit Delancey Street.

–

Merchant Cash Advance Business Debt Relief

Merchant cash advances (MCAs) can provide quick access to capital for small businesses, but they also come with high costs and risks. If your business has struggled to repay an MCA, you may be facing aggressive collection tactics or threats of legal action. However, there are options to resolve MCA debt and protect your business.

How Merchant Cash Advances Work

A merchant cash advance provides a business with a lump sum of capital in exchange for a percentage of future credit card sales. It is not technically a loan, so MCA companies can bypass state lending laws and charge higher fees.Here’s a quick rundown of how merchant cash advances work:

- You receive an upfront sum of cash, usually between $5,000 – $500,000

- The MCA company takes a fixed percentage of your daily credit card sales – typically 8-20%

- You make payments until you pay back the advance plus fees, which often equal a 70-400% APR

- The MCA company can access your credit card receipts to collect payments automatically

This structure allows fast funding but can become problematic if sales drop. You still owe fixed daily payments even if your revenue decreases.

The Risks of Merchant Cash Advances

While MCAs provide easy money upfront, they come with considerable risks:

- Extremely high APRs – MCA fees equate to 70-400% APR on average. This makes costs exponentially higher than business loans or lines of credit.

- Daily payments – You owe fixed daily payments regardless of sales fluctuations, which can quickly become unmanageable. This structure does not accommodate seasonal slowdowns or dips in revenue.

- Aggressive collections – MCA companies can access business bank accounts and credit card receipts to collect payments. Some rely on harassing tactics if you fall behind.

- Personal liability – Business owners often personally guarantee MCA payments. This exposes personal assets if the business struggles.

- Balloon payments – If an MCA is not repaid quickly enough through the fixed percentage deductions, you may owe a large balloon payment of 25-100% of the remaining balance.

As a result of these risky features, many businesses seeking MCA debt relief are facing financial crisis.

Options for Merchant Cash Advance Debt Relief

If your business is overwhelmed by MCA debt, there are options to resolve it and protect your company. Each path depends on your specific situation.

Renegotiate the Advance

If payments are unmanageable but revenue is still reasonably consistent, you may be able to renegotiate terms with the MCA company by:

- Asking to adjust the daily repayment percentage

- Extending the payback term so payments are lower

- Paying a lump sum to reduce principal and associated fees

This requires an open line of communication with the MCA company. Frame renegotiation as a “win-win” to keep the business viable as a source of ongoing payments.

Refinance with More Favorable Financing

If cash flow permits, refinancing high-cost MCA debt can significantly reduce fees. Options to explore include:

- Working capital loans – Banks and alternative lenders provide loans tailored for business operations with rates as low as 5-15% APR.

- Business lines of credit – Lines of credit offer revolving access to capital with interest charged only on what you use. This provides flexibility to adapt to revenue fluctuations.

- Invoice factoring – Invoice factoring converts unpaid customer invoices into immediate capital. Fees range from 1-5% per invoice.

Refinancing spreads payments over longer periods and lowers costs. Lenders can pay off MCAs directly through refinancing packages.

File for Bankruptcy Protection

If debts severely overwhelm revenue, bankruptcy may be the best path to eliminate MCA obligations. Options include:

- Chapter 7 bankruptcy – Liquidates eligible assets to pay creditors. Remaining debts are discharged. Best for businesses closing operations.

- Chapter 11 bankruptcy – Allows reorganization of debts under court protection while keeping business open. The business proposes a repayment plan to creditors.

- Chapter 13 bankruptcy – Like Chapter 11, but for smaller businesses with simpler debts. The business repays debts under a 3-5 year court-approved plan.

The legal process provides breathing room from collections while resolving debts. Bankruptcy damages credit but allows a fresh start.

Attempt Debt Settlement

Debt settlement involves negotiating directly with creditors to pay a lump sum lower than what you owe. This requires:

- Saved settlement funds – You must have lump sum funds, often 20-50% of debt, to pay as settlement. This is difficult for cash-strapped businesses.

- Creditor consent – The creditor must voluntarily agree to accept the reduced payment as full settlement. Many MCA companies reject settlement offers.

If you have sufficient reserves, debt settlement may resolve MCAs for less than face value. But it carries risk of failure.

Finding the Right Solution

With various options to address merchant cash advance debt, it is critical to understand the pros, cons and feasibility of each approach for your unique situation. Key steps include:

- Conducting a detailed financial analysis – Review income statements, balance sheets, accounts receivable/payable, profit margins, seasonal trends, and all short and long-term obligations. This provides clarity on what is sustainable.

- Projecting cash flow at various debt repayment levels – Forecast business cash flow under different scenarios of renegotiated MCA payments, refinancing options, or bankruptcy protection plans. This reveals what is manageable.

- Seeking qualified business debt advice – Consult an attorney and financial specialist to objectively assess your situation and match the right debt relief strategy to your circumstances.

The most appropriate path depends on your revenue and expenses, credit standing, tolerance for business disruption, and prospects for rebuilding after debt resolution. An experienced professional can guide you through the pros, cons and tradeoffs to make an informed decision.

About DeLancey Street

Here at DeLancey Street, we understand the intense stress business owners face when overwhelmed by merchant cash advance debts and aggressive collections. Our dedicated advisors provide judgment-free support to objectively assess your situation and map out customized solutions that make the most financial sense for your company. We help craft strategies to either repay debts in a manageable way or discharge them through legal processes if necessary.If an MCA has your business in crisis, please reach out for a free consultation. We offer transparent guidance at no cost to evaluate the full picture and explain options to relieve financial pressure. Our goal is stabilizing businesses to return focus to growth and profitability. There are always solutions – let us help you find clarity and get your company back on track.

Common Questions about Merchant Cash Advance Debt

Merchant cash advances promise convenient capital but often create spiraling debt. If your business faces overwhelming MCA obligations, you likely have many pressing questions. Here are answers to some frequent concerns:

Can an MCA Company Sue My Business for Repayment?

Yes, an MCA provider can sue your business if you breach the contract terms by missing payments. However, lawsuits are usually a last resort. MCA companies instead rely on accessing your merchant account or business bank account to collect payments automatically through withdrawals. This avoids legal fees.If sued, expect the MCA company to seek immediate full repayment plus extremely high compound interest due to default. They may also request injunctive relief to freeze business assets.Litigation is disruptive and applying full contract terms can sink a business. Seek debt relief support before an MCA company files suit.

Is There a Time Limit for an MCA Company to Sue for Repayment?

Each state has its own statute of limitations dictating deadlines for creditors to sue for repayment. Time limits range between 3-10 years depending on jurisdiction.The “clock” starts either from your last payment or explicit default. If you continue making partial payments, it resets the timeline.Understanding your state’s statute of limitations is useful when weighing options. Once the term lapses, remaining MCA debts become essentially uncollectible through legal means.

Can an MCA Garnish My Wages or Business Accounts?

By obtaining a court judgment, MCA creditors can request wage garnishment pulling payments directly from a business owner’s paycheck. They can also freeze business bank accounts and seize funds.To receive a court order for garnishment, the MCA company must first win a lawsuit proving breach of contract for delinquent payments. This demonstrates formal legal grounds for accessing your income streams and accounts to forcibly collect from outstanding debts.Wage and account garnishment creates massive financial disruption. Seeking relief before judgments occur is critical.

Can I File Bankruptcy on Merchant Cash Advance Debt?

Yes, filing business bankruptcy under chapters 7, 11, or 13 discharges obligations to repay outstanding MCA debts. When approved by court, your business reorganizes finances under bankruptcy protection while halting creditor harassment.MCA companies often argue their products constitute corporate “revenue purchases” rather than loans. But many courts accept MCAs as debt eligible for bankruptcy. Precedent improves odds of discharging MCA obligations without repayment.Bankruptcy damages credit but allows keeping a business operational while developing realistic payment plans. Our advisors help navigate pros, cons and legal process.

The Business Debt Settlement Course

How To Get Out Of Small Business Debt | Small Business Debt Relief Options

Business Debt Settlement can put your small business at risk

Beware Of Business Debt Settlement Companies! #debtsettlement #debt #business #lawfirm

Beware of Business Debt Settlement Scams #debtsettlement #businessdebt #merchantcashadvance

To achieve their development goals, African nations urgently need immediate, unconditional debt relief and quick access to new, low-interest financing, perfectly aligned with the Debt-for-Development swaps concept.

Learn more about the concept from our China Development

中国が債務救済への道を開く

https://gesara.news/china-way-debt-relief/

中国人民銀行は新興市場国の債務再編において債権者間の公平な負担分担を求めており、世界の債務問題に積極的な姿勢を示している。

"After leading Medicaid expansion into becoming a reality, Cooper is pushing and prodding the state’s healthcare systems to help in reducing the $4 billion in medical debt owed by North Carolinians." #ncpol

https://greensboro.com/news/local/governor-touts-churchs-medical-debt-relief-efforts-as-model/article_89276b43-f428-5b0e-b801-8a9a2500ad68.html

Pakistan's finance minister in Beijing to seek debt relief, say sources http://reut.rs/3WBy5dn

Biden/Harris

-Unemp 3.7%, 15M new jobs

- student debt relief,$35 Insulin

-American Rescue Plan,Inflation Reduction Act

-First gun law in 30yrs, Killed AlQaeda head

-Confirmed 200 judges

-Strongest NATO alliance ,New Infrastructure bill

-Secured $1.5B from Mexico

-6Mkidsoutofpover

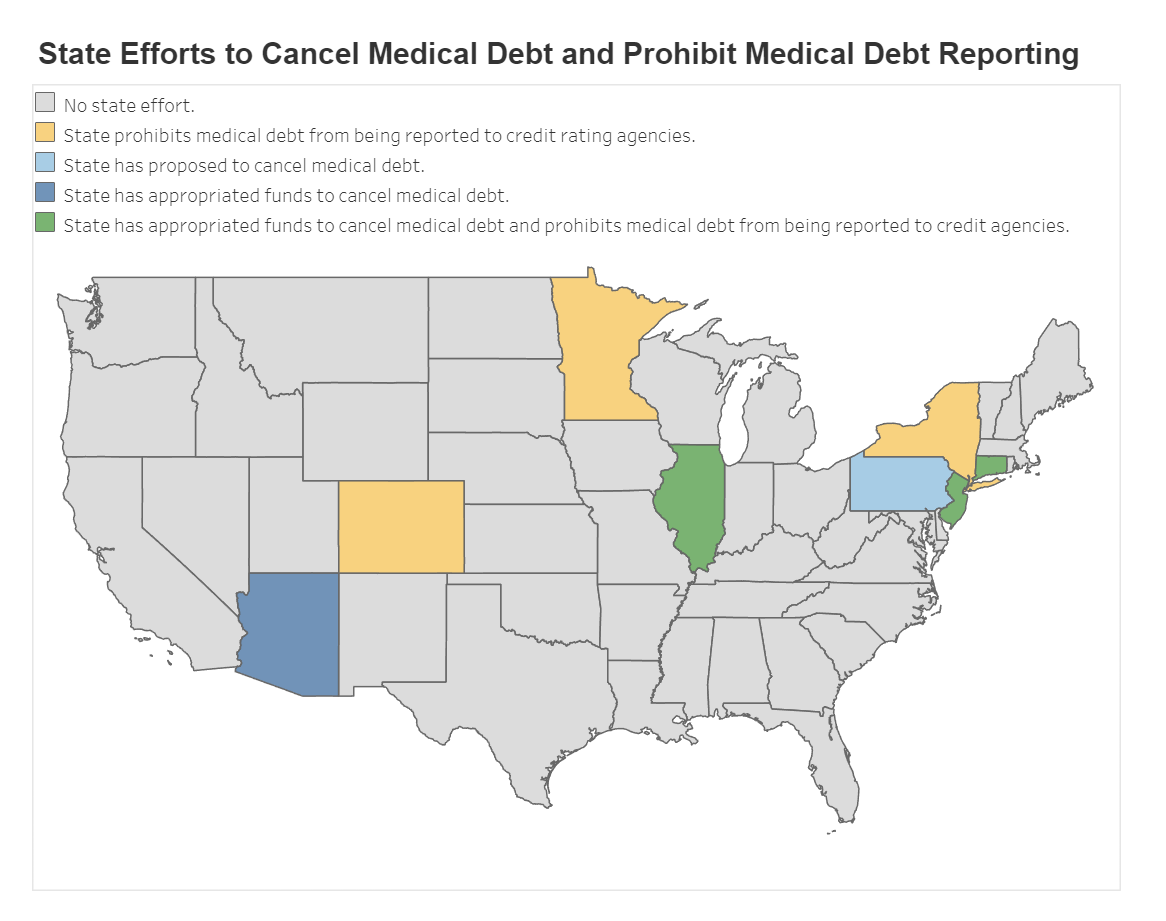

New Jersey is one of only three states in the nation to prohibit medical debt reporting to credit agencies as well as working to provide residents with direct medical debt relief.

We are proud to lead the way in building a health care system that is more affordable and

Student debt relief isn't just a solution; it's a NECESSITY. #CancelStudentDebt

Student debt is a major barrier to #InclusiveGrowth. Let's advocate for affordable education and debt relief programs that allow everyone to thrive. #DebtFreeEducation #GenZ

Last year, we expanded Medicaid, giving more than 600k North Carolinians access to quality, affordable health care. Now, we’re leveraging our Medicaid program to incentivize hospitals to eliminate billions of dollars in medical debt for North Carolinians.

https://www.wbtv.com/2024/07/23/cooper-ncdhhs-hold-round-table-medical-debt-relief/

{kind=link}